E-commerce in APAC is thriving, and the risk of online fraud for consumers is rocketing

Results from Experian’s Digital Consumer Insights 2018 report show that Chinese consumers are the most open to sharing personal data with businesses

Beijing, China, June 13, 2018 — E-commerce in Asia-Pacific is booming – with 71 percent of APAC consumers making an online purchase – but so is the risk of fraud, with one in five customers already falling victim. According to the Report, the demand for online convenience is linked to a heightened threat of fraud. In APAC, 94% of Mainland China consumers are open to reusing their personal data when transacting with new businesses for better convenience or customer experience.

These are among the headline findings of the Digital Consumer Insights 2018, published by the world’s leading information services company Experian, and co-authored with advisory firm IDC.

The report is based on a consumer survey across ten APAC markets namely Australia, China, Hong Kong, India, Indonesia, Japan, New Zealand, Singapore, Thailand and Vietnam. The study delves into how well businesses mitigate fraud risk through the eyes of their most important stakeholders, the customers.

It found that as brands and consumers look for ever-easier ways to buy and sell products online and via mobile devices – with electronics, travel and groceries being the most popular – the opportunity for online fraud is escalating.

Inconvenient truth

The report revealed that almost one in five APAC consumers have already had the misfortune of experiencing fraud.

“Asia Pacific is one of the most dynamic digital and mobile economies in the world,” said Jian Huang, Managing Director of Experian Greater China. “Especially, Mainland China has the highest adoption (around 60%) of mobile payments with the most positive experience with mobile payments. The rapid growth of ecommerce and digital payment initiatives like Alipay and WeChat greatly drive this trend. But as more people adopt faster and more effortless ways to shop, bank and engage with businesses, fraud exposure will increase. This is a concern with 18% of consumers in the region already experiencing fraud while the number exceeds 20% in Mainland China.”

“In APAC, Mainland China consumers are the most open to sharing personal data with businesses if it leads to better services and enhanced fraud detection.” Jian added. “However, compared with the sharing of basic personal data (name, email accounts, and phone numbers), consumers’ willingness to share highly guarded data (biometrics, account numbers, etc.) and demographic information (marital status, income level, age group, etc.) markedly drops. It points out that on one hand, consumers are still not aware enough of the importance of using data to combat fraud and protect their digital identities; on the other hand, it may be led by consumers’ distrust of data reuse between businesses. Relatively speaking, banking institutions and insurance companies enjoy a higher level of consumer trust.”

Meanwhile, consumers have continuous trade-offs between convenience and fraud risk. More than half (51%) of consumers would switch service providers in the event of fraud proving that consumers are willing to trade convenience and a better customer experience for better fraud protection.

The report – a companion to Experian’s Fraud Management Insights 2017, which looked at fraud through the eyes of enterprises – also found distinct differences in consumer attitudes between countries.

In mobile-led, emerging markets, people are more convenience-driven and less risk-averse, with the more security-conscious individuals tending to come from mature economies.

In more mature economies like Hong Kong, consumers are largely more aware of fraud risks and act in a more conservative manner. This means they may sometimes avoid transacting online should they perceive a potential fraud risk. This is, in contrast to emerging economies where consumers are less fraud aware and more convenience driven.

Technology transformation

While the unfortunate reality is that greater digital convenience is linked to higher fraud exposure – presenting a problem for both consumers and businesses – the report also revealed that there was a silver lining.

It found that as consumers became aware of the risk of fraud, they were more likely to want to adopt security measures like biometrics, including fingerprint, facial and voice recognition.

In APAC, 13% of consumers are now willing to adopt biometrics, with India (21%), Vietnam and China (both at 18%) leading the charge as early adopters. Australia (9%), Japan and New Zealand (both at 8%) are the least willing to do so.

Interestingly, however, a significant 57% of consumers are already comfortable with biometrics in government/non-commercial applications.

As acceptance extends into the commercial sphere, this new technology will increasingly be able to provide a more efficient customer experience and enhanced fraud protection.

Data dilemma

At present, one of the best ways companies can protect their customers is by leveraging high-quality customer data to effectively verify transactions.

However, the report found that this was easier said than done.

The findings detailed that consumers were often selective in the type of information they were willing to share with companies, and were clear on how they would want the data to be used.

For example, when asked, 43% of consumers are willing to have their personal data shared with businesses specifically for better fraud detection over convenience or a better customer experience. This number reaches the highest in Mainland China as 56% while HK is only 31%.

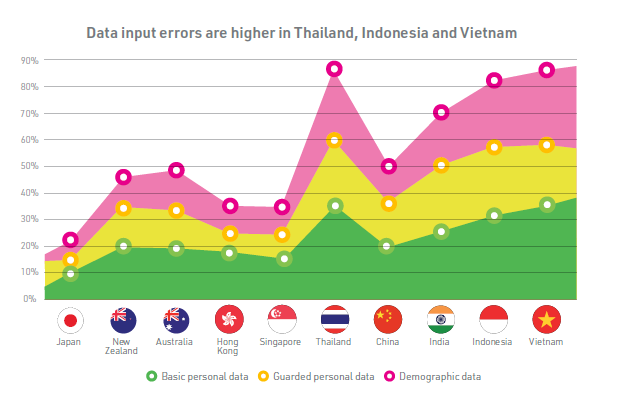

Furthermore, 5% of APAC consumers said they have intentionally submitted inaccurate information to avoid disclosing personal data, while 20% have made mistakes in the details they provided to businesses.

Data input errors were highest in Thailand – while Japan has the lowest erroneous submissions followed distantly by Singapore and Hong Kong.

This points to a gap in trust between businesses and their consumers, but also provides a significant opportunity for them to make improvements. Intentional non-disclosure of information heightens the challenges businesses already face in combatting fraudsters and ascertaining the identity of genuine customers. It is fundamentally an issue of trust – and companies must do more to communicate the value to consumers about the use of data for fraud protection and that they can be trusted as custodians of personal data.